PortsFish.Agency | Trade Intelligence & Data Lab

Predictive Pricing & Volatility Intelligence Layer

Price Index & Forecasting at PortsFish.Agency is a structured analytical framework designed to track, model, and forecast global seafood pricing dynamics across species, regions, corridors, and currency environments.

In international seafood trade, price volatility determines:

- Contract margin stability

- Payment risk exposure

- Inventory strategy

- Trade finance structuring

- Corridor competitiveness

- Capital allocation timing

PortsFish transforms price uncertainty into predictive intelligence.

Strategic Role Within the Ecosystem

The Price Index & Forecasting module integrates with:

- Supply–Demand Analytics

- Market Entry Programs

- Trade Finance & Letters of Credit

- Cross-Border Risk Management

- Investor Intelligence Reports

It provides forward-looking pricing visibility rather than historical reporting.

1. Global Species Price Index

PortsFish tracks structured benchmark pricing for:

- Tuna (fresh / frozen / canned grade)

- Shrimp (by size and origin)

- Salmon (farmed vs wild)

- Whitefish (cod, hake, pollock)

- Cephalopods (squid, octopus)

- Emerging premium species

Each index includes:

- Wholesale benchmark prices

- Import landing prices

- Regional retail averages

- Historical volatility bands

- Currency-adjusted comparatives

The index is updated on a rolling basis depending on market liquidity.

2. Regional Price Benchmarking

Pricing is segmented by:

- United States

- European Union

- GCC

- China

- Japan

- Southeast Asia

- Secondary growth markets

This enables exporters to detect:

- Premium pricing zones

- Price compression regions

- Arbitrage windows

- Cross-market margin discrepancies

3. Volatility & Risk Modeling

Price volatility is driven by:

- Supply shocks

- Climate events

- Fuel and freight costs

- Regulatory tightening

- Trade restrictions

- Currency fluctuations

PortsFish models:

- 12-month rolling volatility index

- Standard deviation bands

- Shock sensitivity modeling

- Corridor-specific volatility multipliers

Volatility intelligence directly informs:

- LC structuring

- Insurance thresholds

- Margin buffers

- Contract renegotiation clauses

4. Forecasting Engine

The Forecasting Layer combines:

- Historical time-series data

- Supply–Demand elasticity modeling

- Seasonality patterns

- Regulatory event projections

- Currency correlation matrices

- Freight & fuel cost overlays

Forecast windows include:

- Short-term (30–90 days)

- Medium-term (6 months)

- Annual projection (12 months)

Confidence intervals are displayed to indicate forecast reliability.

5. Scenario Modeling Lab

Investors and exporters can simulate scenarios such as:

- 20% fuel price increase

- EU quota reduction

- Sudden port congestion spike

- Currency devaluation event

- Regulatory tightening in IUU enforcement

- Climate-driven production disruption

The system recalculates:

- Price impact

- Margin compression risk

- Corridor attractiveness shifts

- Risk-Adjusted Opportunity Index (RAOI) changes

6. Margin Impact Dashboard

Price forecasting integrates with:

- Freight cost trends

- Insurance premiums

- Cold chain operational costs

- FX hedging exposure

- Import duty shifts

This provides:

- Net export margin outlook

- Corridor-level profitability forecast

- Risk-adjusted pricing recommendations

7. Investor & Bank View

For institutional users, the module provides:

- Volatility-adjusted corridor ranking

- Price stability score

- FX sensitivity heatmap

- Capital exposure alerts

- Structured commodity financing signals

Banks can use this intelligence to adjust:

- Spread pricing

- Collateral requirements

- LC confirmation thresholds

- Trade credit insurance mandates

8. Alerts & Early Warning Signals

The system generates alerts for:

- Price breakout beyond volatility band

- Rapid demand surge

- Supply compression signals

- Regulatory-driven scarcity

- Currency shock impact

- Corridor re-pricing shifts

Alerts can be delivered via:

- Dashboard notification

- Email brief

- Institutional bulletin

9. Integration with Risk & Finance Systems

Price Index & Forecasting feeds into:

- Customs Risk Scoring Model (CRSM)

- International Payment Risk Scoring Matrix (IPRSM)

- Cross-Border Risk Index (CBRI)

- Supply–Demand Analytics

- Investor Intelligence Reports

Pricing intelligence influences:

- Payment mechanism selection

- Contract length decisions

- Hedging strategies

- Corridor selection

- Working capital allocation

10. Strategic Outcome

Price Index & Forecasting transforms seafood pricing from reactive contract negotiation into predictive, risk-adjusted financial planning.

The objective is:

• Anticipate price movement

• Protect margins

• Reduce volatility exposure

• Optimize corridor strategy

• Strengthen negotiation power

• Align trade finance with pricing cycles

PortsFish does not simply report prices.

It models pricing behavior within structured global trade systems.

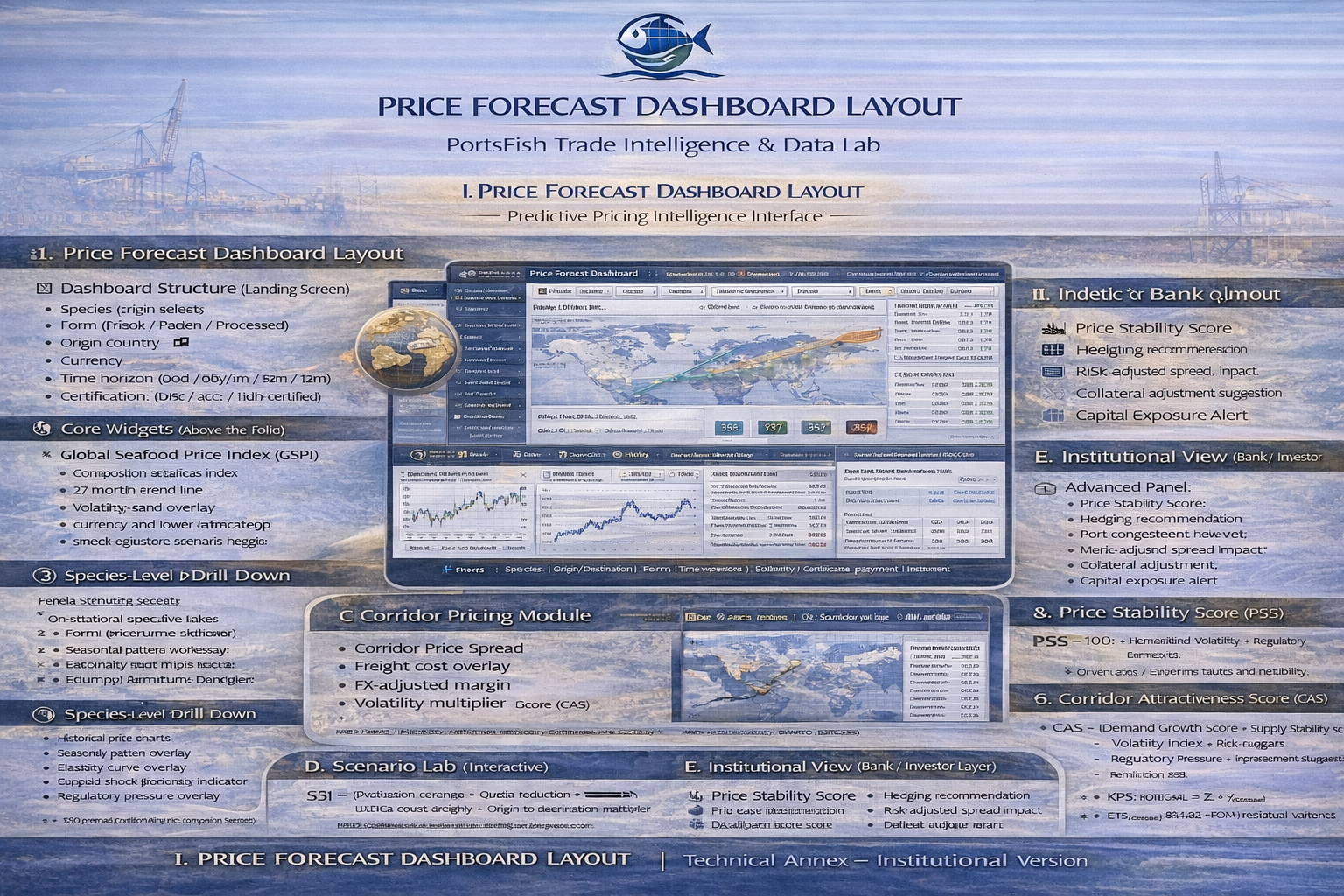

I. PRICE FORECAST DASHBOARD LAYOUT

PortsFish Trade Intelligence & Data Lab

Predictive Pricing Intelligence Interface

1️⃣ Dashboard Structure (Screen-by-Screen Layout)

A. Global Price Overview (Landing Screen)

Top Bar Filters

- Species (multi-select)

- Form (Fresh / Frozen / Processed)

- Origin country

- Destination market

- Currency

- Time horizon (30d / 90d / 6m / 12m)

- Certification (MSC / ASC / Non-certified)

- Incoterm

Core Widgets (Above the Fold)

- Global Seafood Price Index (GSPI)

- Composite weighted index

- 12-month trend line

- Volatility band overlay

- Forecast Curve

- Baseline projection

- Upper and lower confidence bands

- Shock-adjusted scenario toggle

- Volatility Gauge

- Current volatility percentile (vs 5-year history)

- Color-coded: Green / Amber / Red

- Margin Risk Indicator

- Corridor-specific margin compression probability

B. Species-Level Drill Down

Panels:

• Historical price chart (1Y / 3Y / 5Y)

• Seasonal pattern overlay

• Elasticity curve

• Supply shock sensitivity indicator

• Regulatory pressure overlay

Right Panel:

• Price Forecast Table (30d / 90d / 6m / 12m)

• Forecast confidence score

• FX impact sensitivity

C. Corridor Pricing Module

Map-based interface:

Origin → Destination

Metrics:

- Corridor Price Spread

- Freight cost overlay

- FX-adjusted margin

- Volatility multiplier

- Corridor Attractiveness Score (CAS)

D. Scenario Lab (Interactive)

User can toggle:

- Fuel +20%

- EU quota reduction

- Port congestion event

- Currency shock (±10%)

- Regulatory tightening

- Supply disruption event

System recalculates:

- Forecast curve

- Margin compression

- Volatility index

- Recommended payment instrument

E. Institutional View (Bank / Investor Layer)

Advanced Panel:

- Price Stability Score

- Hedging Recommendation

- Risk-adjusted spread impact

- Collateral adjustment suggestion

- Capital exposure alert

II. INDEX CALCULATION METHODOLOGY

Technical Annex – Institutional Version

1️⃣ Global Seafood Price Index (GSPI)

1.1 Index Structure

GSPI = Σ (Wi × Pi_adj)

Where:

Wi = weight of species i (based on global trade volume share)

Pi_adj = currency and corridor adjusted price of species i

Weights recalculated annually based on:

- Global trade volume

- Value-weighted trade flows

- Liquidity of market data

1.2 Currency Adjustment

Pi_adj = Pi_local × FX_normalization_factor

FX_normalization_factor adjusts all prices into USD baseline using rolling FX average.

2️⃣ Volatility Index (VI)

VI = σ(Pt − Pt-1) × √252

Where:

σ = standard deviation

252 = trading days annualization factor

Volatility percentile = current VI vs 5-year rolling distribution.

3️⃣ Forecasting Engine

Hybrid Model:

A. Time-Series Core

ARIMA / SARIMA (seasonal adjustment)

B. Exogenous Variables

Regression layer including:

- Fuel index (Brent)

- Freight index

- FX rate

- Regulatory pressure score

- Supply Shock Indicator (SSI)

Forecast:

Pt+1 = α + β1(Fuel) + β2(Freight) + β3(FX) + β4(Regulatory) + β5(SSI) + ARIMA_component

4️⃣ Supply Shock Indicator (SSI)

SSI = (Production variance + Quota reduction + Climate event weight) × Origin concentration multiplier

Scaled 0–100.

5️⃣ Regulatory Pressure Score (RPS)

RPS = (IUU enforcement intensity + SPS alert count + Anti-dumping exposure) weighted by destination market severity.

6️⃣ Margin Compression Probability (MCP)

MCP = f(Price Volatility, Freight % of price, FX deviation, Inventory pressure)

Logistic regression model outputs:

Probability (0–1) of margin falling below defined threshold.

7️⃣ Confidence Interval Calculation

CI = Forecast ± (Z × σ_forecast)

Z = 1.96 for 95% CI

σ_forecast derived from residual variance.

8️⃣ Price Stability Score (PSS)

PSS = 100 − (Normalized Volatility × Regulatory multiplier)

Higher score = lower structural instability.

9️⃣ Corridor Attractiveness Score (CAS)

CAS = (Demand Growth Score × Supply Stability Score)

− (Volatility Index × Risk Weight)

− (Regulatory Pressure × Enforcement Multiplier)

Normalized 0–100.

III. STRATEGIC VALUE

This system allows:

• Banks to adjust LC confirmation thresholds

• Exporters to time contracts

• Importers to hedge properly

• Investors to allocate capital based on volatility-adjusted yield

• Ports to anticipate volume shifts

This is not a price chart.

It is a pricing intelligence engine embedded inside a trade infrastructure system.