(Regulated Transactional Control & Territorial Execution Framework)

Institutional Definition

Local Sales Execution Authority (LSEA) is the legally recognized, territorially regulated execution function delegated exclusively to the appointed City Partner, granting them full responsibility for licensed brokerage activity, transactional negotiation, contract execution, regulatory compliance, and closing coordination within their jurisdiction.

REFD centralizes structure.

The City Partner holds execution authority.

This separation preserves regulatory legitimacy and prevents structural conflict.

I. Conceptual Foundation

In global real estate markets:

- Brokerage activity is locally regulated.

- Licensing is jurisdiction-specific.

- Contract law varies per territory.

- Compliance requirements differ significantly.

Attempting centralized transaction control creates:

- Regulatory exposure

- Licensing violations

- Market resistance

- Anti-monopoly concerns

- Operational inefficiency

Therefore, transactional authority must remain local.

II. Structural Objective

The purpose of Local Sales Execution Authority is to:

- Preserve legal compliance

- Protect structural neutrality

- Avoid licensing conflict

- Ensure transactional efficiency

- Maintain market legitimacy

- Enable scalable international expansion

Execution is territorial.

Structure is centralized.

III. Scope of Authority

The Exclusive City Partner holds authority over:

- Property listing validation

- Seller representation agreements

- Buyer representation agreements

- Negotiation management

- Contract drafting (as per local law)

- Escrow coordination

- Regulatory filings

- Closing execution

- Commission collection

- Post-sale compliance reporting

REFD does not interfere in regulated brokerage activity.

IV. Functional Separation Matrix

| Function | REFD | City Partner |

|---|---|---|

| Asset Qualification | ✔ | Input support |

| Architectural Repositioning | ✔ | Data support |

| Financial Modeling | ✔ | Market data input |

| Risk & SPV Structuring | ✔ | Compliance coordination |

| Capital Activation | ✔ | Local investor facilitation |

| Negotiation | ✖ | ✔ |

| Contract Execution | ✖ | ✔ |

| Regulatory Filing | ✖ | ✔ |

| Closing | ✖ | ✔ |

This separation prevents overlap and liability exposure.

V. Regulatory Compliance Framework

The City Partner must:

- Hold valid brokerage license

- Maintain regulatory standing

- Carry professional liability insurance

- Comply with local consumer protection law

- Comply with anti-money laundering (AML) standards

- Maintain escrow compliance where applicable

Failure results in revocation of exclusivity.

VI. Transaction Integrity Protocol

To ensure systemic discipline:

- All structured projects must be pre-registered in REFD system

- Revenue participation schedule must be documented before execution

- Commission breakdown must be reported post-closing

- Attribution of lead origin must be recorded

Transparency prevents conflict.

VII. Revenue Execution Flow

Transaction execution follows this sequence:

- Buyer identified (local or REFD-generated)

- Negotiation conducted by City Partner

- Agreement executed under local law

- Commission collected by City Partner

- Structural participation allocated per pre-agreed terms

- Reporting submitted to REFD

REFD does not collect commission unless legally structured.

VIII. Legal Risk Containment

Local Sales Execution Authority protects REFD from:

- Licensing liability

- Brokerage malpractice claims

- Escrow disputes

- Local regulatory penalties

- Misrepresentation claims

Liability remains localized within jurisdiction.

IX. Anti-Monopoly Safeguard

Because REFD:

- Does not transact locally

- Does not control brokerage license

- Does not negotiate contracts

- Does not collect base commission

The system cannot be classified as brokerage monopoly.

It operates as structural infrastructure.

X. Conflict Resolution Mechanism

In case of:

- Revenue dispute

- Attribution conflict

- Contractual disagreement

- Performance under-delivery

Resolution follows:

- Internal review

- Governance Committee mediation

- Arbitration (if required)

Structured protocol prevents reputational escalation.

XI. Performance Monitoring

City Partner execution is evaluated based on:

- Transaction velocity

- Conversion efficiency

- Compliance adherence

- Reporting discipline

- Governance cooperation

Exclusivity is conditional.

XII. Strategic Advantages of Local Execution Model

- Legal compliance stability

- Cultural and market familiarity

- Faster negotiation cycles

- Reduced regulatory friction

- Capital-light expansion

- Clear accountability structure

It is operationally efficient and legally protected.

XIII. Comparative Market Positioning

| Centralized Brokerage Expansion | Marketplace Portal | REFD Local Execution Model |

|---|---|---|

| Licensing complexity | Structurally weak | Structurally strong |

| High fixed cost | Low structural depth | Balanced architecture |

| Regulatory exposure | Minimal control | Clear separation |

| Competitive | Neutral | Cooperative |

REFD occupies a hybrid institutional position.

XIV. Scalability Implications

Because execution is local:

- No need for global licensing

- No need for branch offices

- No direct payroll expansion

- No regulatory multi-jurisdiction liability

Global scalability becomes feasible.

XV. Governance & Oversight Integration

Local Sales Execution Authority operates within:

- IP Safeguard Annex

- Revenue Sharing Annex

- Governance Charter

- Capital Engineering Handbook

All execution must adhere to structural standards.

XVI. Institutional Conclusion

Local Sales Execution Authority establishes a legally compliant, territorially grounded, execution layer that preserves regulatory integrity while enabling centralized structural intelligence to scale globally.

It ensures:

- Legal immunity

- Market legitimacy

- Revenue alignment

- Governance discipline

- Structural neutrality

- Scalability

REFD builds structure.

City Partners execute transactions.

This is the backbone of regulatory resilience.

REAL ESTATE FASHION DIGITAL (REFD)

MASTER GOVERNANCE WHITE PAPER

(Structural Intelligence, Capital Engineering & Territorial Execution Framework)

I. Institutional Declaration

Real Estate Fashion Digital (REFD) is a structured capital engineering infrastructure designed to transform real estate assets into calibrated, risk-adjusted, capital-aligned investment instruments through centralized structuring intelligence and decentralized regulated execution.

REFD monetizes structure, not listings.

This White Paper establishes the governance, operational, legal, financial, and territorial frameworks ensuring institutional durability, neutrality, and global scalability.

II. Foundational Principles

- Structural centralization

- Local execution decentralization

- Incentive alignment

- Regulatory compliance

- Capital discipline

- Risk isolation

- Performance-based exclusivity

- Governance continuity independent of individuals

III. Structural Architecture Overview

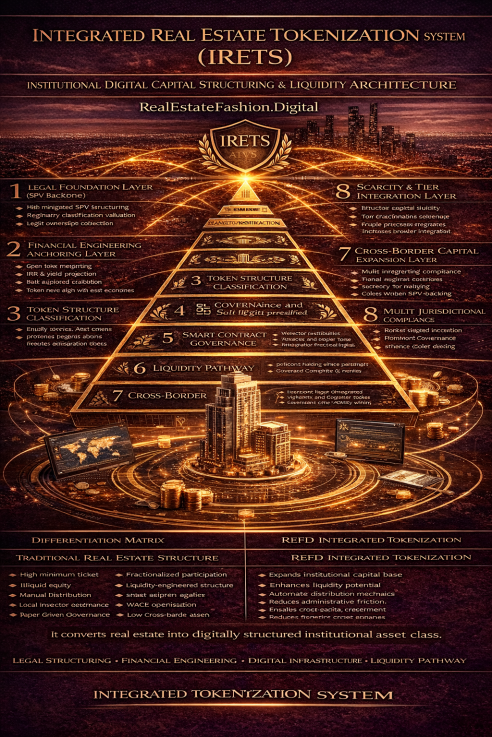

The REFD system operates across five integrated layers:

- Asset Qualification

- Architectural Repositioning

- Financial Modeling & Capital Alignment

- Risk Architecture & SPV Structuring

- Structured Financing Pathways

These layers form the Capital Engineering Infrastructure.

IV. City Representation Model

A. Structural Central Authority (REFD)

REFD retains authority over:

- Qualification Protocols

- Repositioning Methodology

- Financial Engineering Standards

- Risk Architecture Framework

- Capital Stack Design

- Portfolio Aggregation Logic

- Governance Standards

All structural methodologies remain centralized intellectual property.

B. Local Sales Execution Authority (LSEA)

The Exclusive City Partner holds regulated transactional authority within jurisdiction.

Scope includes:

- Listing agreements

- Buyer-seller negotiation

- Contract drafting under local law

- Escrow management

- Regulatory filings

- Closing execution

- Commission collection

REFD does not conduct brokerage activity.

Execution is territorial.

Structure is centralized.

V. Functional Separation Matrix

| Function | REFD | City Partner |

|---|---|---|

| Asset Structuring | ✔ | Support |

| Architectural Optimization | ✔ | Data input |

| Financial Modeling | ✔ | Market input |

| Risk & SPV | ✔ | Compliance coordination |

| Capital Activation | ✔ | Facilitation |

| Negotiation | ✖ | ✔ |

| Contract Execution | ✖ | ✔ |

| Regulatory Compliance | ✖ | ✔ |

| Commission Handling | ✖ | ✔ |

This separation prevents regulatory exposure and preserves neutrality.

VI. Revenue Governance Framework

Revenue is event-based and performance-aligned.

Revenue categories:

- REFD-originated structured assets

- City-originated structured assets

- Telesales-generated transactions

- Portfolio / bundle participation

Revenue distribution requires:

- Pre-agreed participation schedule

- Lead attribution documentation

- Post-closing reporting

- Transparent reconciliation

No subscription model.

No franchise extraction.

VII. Risk Architecture Framework

Risk is categorized and isolated:

| Risk Type | Controlled By |

|---|---|

| Regulatory Risk | City Partner |

| Construction Risk | Structured modeling |

| Market Risk | Sensitivity testing |

| Capital Risk | Stack engineering |

| Portfolio Risk | Aggregation modeling |

SPV structures prevent cross-liability contamination.

VIII. Legal Protection & IP Safeguard

REFD protects:

- Qualification frameworks

- Modeling templates

- Capital stack algorithms

- Risk architecture methodologies

- Portfolio integration systems

City Partners receive usage rights only.

Non-replication, non-circumvention, and confidentiality clauses apply.

Structural continuity is preserved independent of individuals.

IX. Governance & Oversight Structure

The Governance Framework includes:

1. Central Structural Authority

Maintains modeling, capital, and risk standards.

2. City Partner Oversight

Evaluated quarterly on:

- Compliance

- Reporting discipline

- Transaction velocity

- Structural cooperation

3. Governance Committee

Responsible for:

- Performance audits

- Exclusivity confirmation

- Conflict mediation

- Structural amendment approval

No unilateral authority exists.

X. Anti-Monopoly & Neutrality Clause

REFD:

- Does not hold brokerage license

- Does not transact directly

- Does not restrict market access

- Does not centralize regulatory authority

It operates as structural infrastructure layer, not brokerage operator.

This preserves competitive neutrality.

XI. Scalability Framework

Scalability is achieved through:

- One Exclusive City Partner per city

- Centralized modeling intelligence

- Decentralized licensed execution

- Capital-light expansion

- Modular capital stacking

- Portfolio bundling capability

Global expansion does not require branch licensing.

XII. System Continuity & Institutional Durability

To ensure immunity from personal dependency:

- All processes documented

- Governance committee oversight

- Structural IP centralized

- Revocation and replacement protocols defined

- Capital engineering standardized

The system must survive leadership transition.

XIII. Structured Financing Integration

Financing architecture includes:

- Capital source mapping

- Tier calibration

- Stack engineering

- Jurisdictional optimization

- Phased deployment

Capital is engineered, not improvised.

XIV. Portfolio & Capital Corridor Strategy

REFD enables:

- Multi-Asset Bundles

- Urban Strategic Nodes

- Intercontinental Operations

- Blended IRR portfolio construction

- Cross-border capital corridors

Assets become components of engineered portfolios.

XV. Compliance & Reporting Discipline

Mandatory documentation per project:

- Qualification Summary

- Architectural Repositioning Report

- Financial Engineering Memorandum

- SPV & Risk Architecture Document

- Capital Alignment Profile

- Financing Memorandum

- Sensitivity Annex

Transparency precedes capital deployment.

XVI. Institutional Positioning

REFD occupies the structural layer between:

- Local brokerage execution

- Institutional capital allocation

It integrates:

Design

Finance

Risk

Governance

Territorial execution

Within a unified capital engineering infrastructure.

XVII. Institutional Conclusion

The REFD Master Governance White Paper codifies:

- Structural intelligence centralization

- Regulated local execution

- Incentive-aligned revenue architecture

- Risk isolation via SPV

- Capital tier alignment

- Governance discipline

- Institutional scalability

It establishes REFD as:

A Capital Structuring Infrastructure

Not a Brokerage Platform

Not a Marketplace

Not a Fund

But a structured capital engineering system capable of global territorial deployment while preserving regulatory legitimacy and structural immunity.